Topic 1: FESTIVE WITH FRET: AUGUST 2024

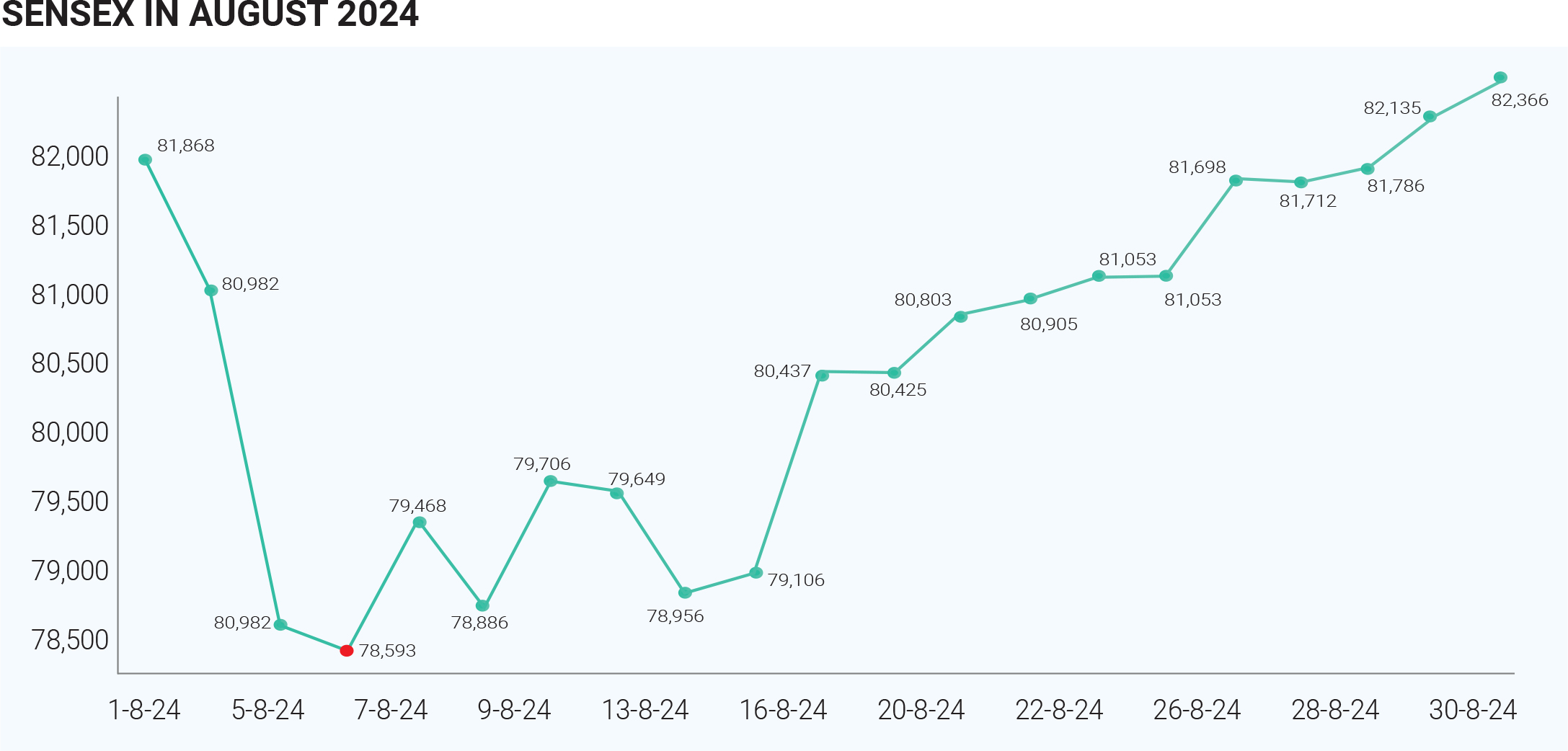

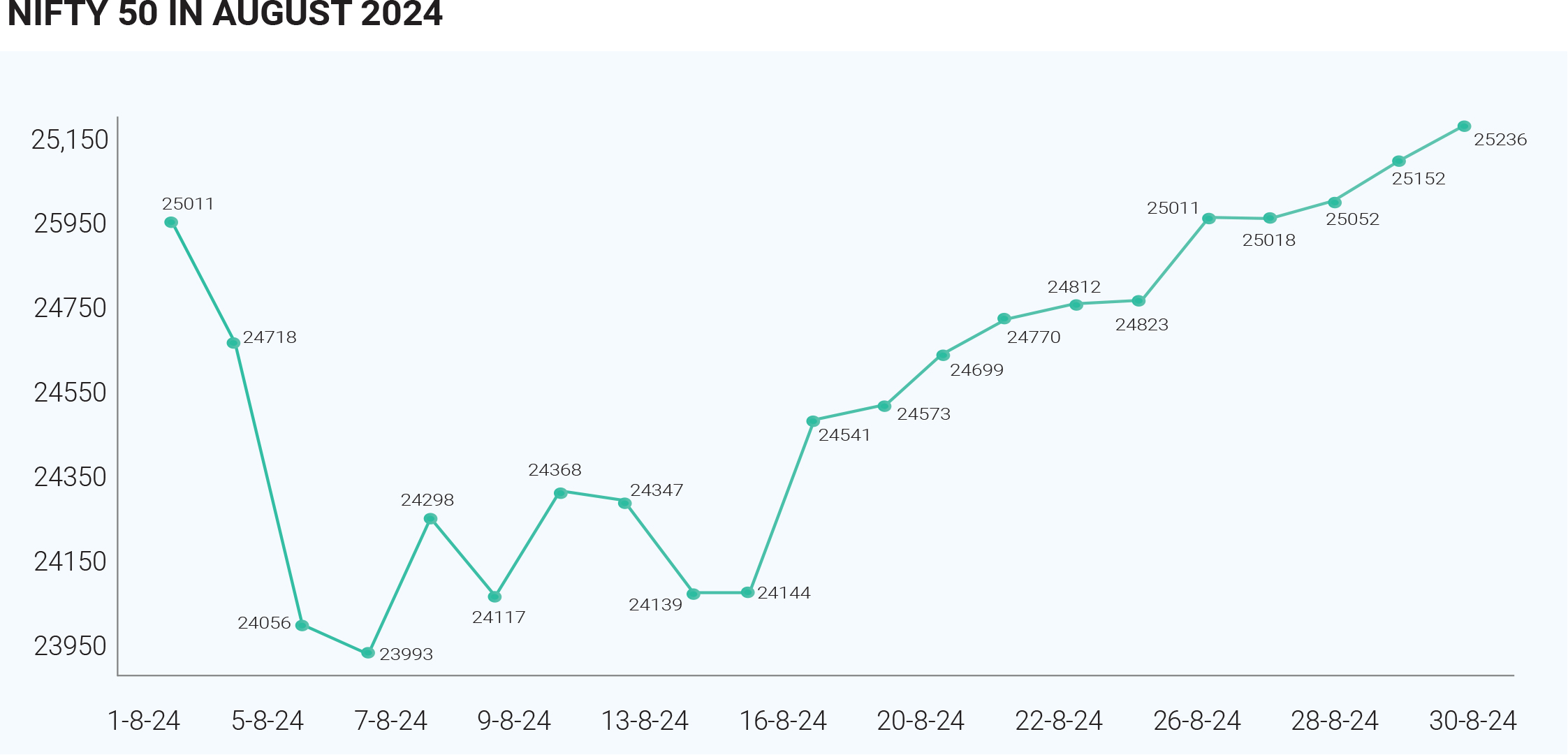

The Indian markets after the interim budget exhibited strong performance touching multiple record highs in the month of August 2024. The Nifty 50 and the Sensex performed exceptionally well, reaching record highs by the end of the month. Nifty 50 closes at 25,235.90 points, marking a gain of 83.95 points or 0.33% whereas Sensex ended at 82,365.77 points, up by 231.16 points or 0.28%. So the markets moved in the positive territory over the month, attributed to the robust foreign investment inflows, positive corporate earnings reports, and favourable economic data, which bolstered investor confidence. Initially in the month, economic data from major economies, particularly the US, China, and Japan, played a significant role. Weak economic indicators, such as a disappointing US jobs report and concerns about the Chinese economy, initially led to a decline in the Sensex early in the month, causing it to drop over 2,000 points on August 5. Then later in the month anticipation of a potential interest rate cut by the U.S. Federal Reserve contributed to positive market sentiment. Investors were optimistic that easing monetary policy could support economic growth, bolstering the Indian markets. This factor also contributed to the notable increase in foreign fund inflows which enhanced investor confidence and moved the markets in an upward trajectory. Sectors which particularly showed strong performance are IT and consumer goods. The market saw significant contributions from stocks like Cipla, Bajaj Finance, Mahindra & Mahindra, Divis Lab, and NTPC.

Looking at the Indian debt market which also exhibited a positive performance in August 2024, with yields declining and liquidity improving. The yield on the 10-year government bond decreased from 7% at the start of August to 6.92% by the end of the month. The yield curve steepened as short-term G-Sec yields decreased more than longer-term yields. Corporate bond market yields also fell, reflecting positive sentiment from the sovereign bond market. The debt market saw increased liquidity in the interbank market, leading to overnight rates trading at the lower end of the repo rate corridor. This shift in liquidity impacted the other segments of the money market curve, resulting in a decline in money market yields across the board. The factors which affected the yields are mainly a low fiscal deficit of 4.9% of GDP for FY 2025, high net inflows in the last month due to inclusion of Indian G-Sec in JP Morgan emerging markets bond index and lastly expectations of US Fed rate cut in September 2024 due to US Inflation data. 10-year G-Sec yield is expected to maintain a downward bias trend and may eventually drift towards the Marginal Standing Facility (MSF) rate. The Indian debt market exhibited a favourable performance in August 2024, characterized by declining yields, improved liquidity conditions, and positive global cues. In August 2024, the trend of Foreign Institutional Investors (FIIs) in India showed significant volatility, characterized by a sharp reversal in investment patterns during the month. The first half of August (August 1-14) witnessed substantial outflows, with FIIs selling equities worth approximately $2.12 billion. This marked the highest outflow among emerging markets during this period, leading to declines of over 1% in both the Sensex and Nifty indices, and even larger drops in the BSE MidCap and SmallCap indices. In contrast, from August 16 to 27, FIIs reversed their stance, pouring over $1.6 billion into Indian equities. This influx was largely driven by bulk deals in major companies such as Ambuja Cement and Tata Tech, contributing to a recovery in the benchmark indices, which rose by more than 1.4% during this period. Despite the late-month buying spree, the overall net position for FIIs in August remained negative, with total sales amounting to approximately ₹16,304 crore (around $2 billion) by the end of the month. This reflects a cautious approach from FIIs, who have been selective in their investments. Since this year Gold prices have been in a positive zone due to geopolitical uncertainties, elections in major world economies, and continuous fragmentation of the world economies too. The first half of August saw gold prices move up by more than $80, touching a fresh all-time peak of $2,525 per ounce. However, the second half of the month showed reduced uncertainty, mainly concerning the timing of rate cuts amidst a backdrop of signs of slowing inflation. This led to gold prices ending August at $2,503 per ounce, still a gain of approximately 2.4% for the month. Domestic gold prices in India also moved up by around 2.4% mainly due to global gold price trends. The revision of the import rate cut on Gold in Interim Budget 2024 has pressurised the prices for a short period, but the medium-term outlook for the precious metal remains promising, given the imminent turn in the US interest rate cycle and the confluence of macroeconomic factors impacting growth and markets. Looking at the currency market Indian Rupee depreciated by 0.2% against the USD closing at Rs83.87 per dollar, this pulled down the rupee into the worst-performing Asian currency for the month. Throughout August, the rupee fluctuated within a narrow range, with notable trading levels around ₹83.70 to ₹84.05. The Reserve Bank of India (RBI) played a significant role in stabilizing the currency by intervening in the market to prevent it from crossing the 84 mark. In August 2024, the Indian rupee experienced a slight depreciation of 0.2% against the US dollar, closing the month at approximately ₹83.87 per dollar. This performance made the rupee the second-worst-performing Asian currency for the month, following the Bangladeshi taka. Despite a general weakening of the US dollar, the rupee's decline was attributed to increased demand for dollars from importers and reduced foreign portfolio investment (FPI) inflows, particularly in the equity market. Throughout August, the rupee fluctuated within a narrow range, with notable trading levels around ₹83.70 to ₹84.05. The Reserve Bank of India (RBI) played a significant role in stabilizing the currency by intervening in the market to prevent it from crossing the 84 mark. Indian Rupee moves in a narrow range due to factors like strong demand for USD from importers, net outflows of FIIs from equity markets, widening trade deficit as imports are more than exports and lastly geopolitical uncertainties favour USD demand. The global economic instability would keep the currency vulnerable against the USD. The depreciating rupee hurts crude oil prices in India, and with the increasing import costs of crude oil import bill will inflate. The early August 2024, crude oil prices saw an increase, however in the last week of August is fell sharply by 3.48%, which earned all the profits for the year to date. Crude oil prices declined due to OPEC+ preparing for increased production in October, the economic slowdown faced by many major countries and lastly Libya's resolution to restore the output. Overall, the high price of crude oil in August 2024 acted as a catalyst for the rupee's decline, highlighting the vulnerability of the Indian economy to fluctuations in global oil prices. In September 2024, investors should take care of the development of domestic and global conditions. On the domestic front, inflation numbers could lead the markets and currency, corporate numbers would be crucial, monsoon effect, festive season spending, and the decline of FII investments could keep the markets volatile. The global factors contributing to the market trend would include US monetary policy decisions, global economic indicators and ongoing geopolitical conflicts, which will play a crucial role for the investor. Investors should remain vigilant and consider these factors when making investment decisions.